Contents

Similarities between Commercial Banks and NBFIs:

Non-Scheduled Banks of Bangladesh:

Scheduled Banks of Bangladesh

The financial market in Bangladesh

Regulators of the Financial System

Capital Market

Recent Developments in Financial Sector in Bangladesh

Insurance

NBFI

CAMELS

What Is Market Risk?

What Is a Nonperforming Loan?

What is Funds Management

Liquidity Management in Business and Investing

What is Prime Security and Collateral Security?

Primary Security vs Collateral Security

**What is an Offshore Banking Unit (OBU)

**What Is Positive Pay?

What Is Stress Testing?

What Is a Bank Rate?

What Is the Interest Rate Spread?

What Is Cost of Funds?

What Is Core Capital?

Shell bank

What Is Reputational Risk?

Compare Branch Banking VS Unit Banking

What Is a Smurf or Structuring?

What is a Lien

What Is a Set-Off Clause?

What Is Asset/Liability Management?

What is a Classified Loan?

What Is a Loan Loss Provision?

What Is a Beneficial Owner?

Funded & Non-Funded Loan: Definition, Uses etc.

Relationship between Banker and Customer

Politically exposed person (PEP)

False positive

What Is Trust Receipt?

Due diligence

Enhanced due diligence (EDD)

What Is a Suspicious Activity Report (SAR)?

Currency Transaction Report (CTR)

KYC

CTR

STR

KYC - Know Your Customer (Banking) and KYE

RTGS

National Payment Switch Bangladesh (NPSB)

Automated Teller Machines (ATM):

Point of Sales (POS):

Internet Banking Fund Transfer (IBFT):

Payment systems in BB

Mobile Financial Services (MFS)

Payment Service Provider (PSP) and Payment System

Operator (PSO)

BFIU

What Is Electronic Commerce (e-commerce)?What Is Return

on Equity – ROE?

What Is Return on Assets—ROA?

The return on revenue (ROR)

What Is Value at Risk (VaR)?

What is Capital Adequacy Ratio – CAR?

What Is Earnings Per Share?

What Is a Cryptocurrency?

Magnetic Ink Character Recognition (MICR) Line?

Trade-Based Money Laundering (TBML)

What Is Basel II?

What Is Basel III?

Legacy Account

Mutual Evaluation

Credit Deposit Ratio

Different types of Account

Credit Documentation

Recover Classified Loans

Self-Assessment Report

Agent Banking

SME Financing

Similarities between Commercial Banks and NBFIs:

From a functional viewpoint the operations of commercial

banks are similar to those of NBFIs on the following counts:

1. Like NBFIs, commercial banks acquire the primary

securities of borrowers, loans and deposits, and in turn, they provide their

own indirect securities and demand deposits to the lenders. Commercial banks

resemble NBFIs in that both create secondary securities in their role as

borrowers.

2. Commercial banks create demand deposits when they borrow

from the central bank, and NBFIs create various forms of indirect debt when

they borrow from commercial banks.

3. Both commercial banks and NBFIs act as intermediaries in

bringing ultimate borrowers and ultimate lenders together and facilitate the

transfer of currency balances from non-financial lenders to non-financial

borrowers for the purpose of earning profits.

4. Both commercial banks and NBFIs provide liquid funds. The

bank deposits and other assets of commercial banks and the assets provided by

NBFIs are liquid assets. Of course, the degree of liquidity varies in

accordance with the nature and the activity of the concerned financial

intermediaries.

5. Both banks and NBFIs are important creators of loanable

funds. The commercial banks by net creation of money and the NBFIs by

mobilising existing money balance in exchange for their own newly issued

financial liabilities.

Difference between Commercial Banks and NBFIs?

Commercial banks are different from NBFIs in the following

respects:

1.

Credit Creation:

Prof. J. Tobin has shown that the existence of NBFIs

significantly modifies the conventional view of commercial banks as creators of

money because they can directly issue their own new liabilities to acquire

other assets. On the other hand, NBFIs do not create money.

Like all other financial intermediaries (FIs), commercial

banks lend to borrowers only currency deposited with them and make profit by

charging borrowers a high rate than they pay to lenders. But both differ in the

effects of their operations so far as secondary securities are concerned.

The two main financial assets that serve as money are

currency, known as high powered money, and demand deposits of commercial banks.

Demand deposits are the secondary securities issued by commercial banks which

are substitutes for currency.

They represent a promise to pay currency on demand and are

transferred direct by cheque without encashment in settlement of debt. Banks

offer convenient safe-keeping, book-keeping and a large number of other services

to depositors that are not available by holding currency.

Consequently, depositors who lend their currency to

commercial banks receive in return a secondary security that itself serves as a

medium of payment. Loans made or deposits created by any bank through the issue

of cheques will ultimately be deposited by the borrowers or by other persons to

whom they made cheque payments in the commercial banking system. Thus cheques

help in creating credit by the bank credit multiplier.

Money lent by an individual bank is retained as cash reserve

by the banking system minus only a small leakage in money used by the borrower.

The bank credit multiplier implies that banks if uncontrolled would have an

unlimited power to expand deposits, since the latter are determined only by the

amount of primary securities that the banking system purchases.

“Bank money, once created in the process of bank lending,

lives on as a virtually permanent part of the money supply. Thus, banks do

manufacture money; and once manufactured, it is relatively immortal.” It is in

this sense that commercial banks are unique among FIs in their ability to

create money. But in the case of NBFIs, the amount of primary securities they

can buy is limited by the amount of indirect securities they can sell to

lenders.

Since they do not possess the bank credit multiplier power

of commercial banks, they perform the brokerage function of simply transferring

to borrowers the funds entrusted to them by lenders. Moreover, government

regulations prevent NBFIs from offering chequing facilities on their

liabilities and convertibility into currency on demand.

But a number of secondary securities, such as commercial

bank time and demand deposits and deposits in some thrift institutions while

directly not transferable by cheque can be turned into cash quickly, easily,

conveniently and without cost. Therefore, they are a close substitute of money

than other assets, are called near money assets.

Thus NBFIs can create liquidity and not money. Since the

majority of NBFIs are small, the banking system multiplier does not operate

fully in their case because of the leakages to banks of the money lent. Suppose

a small non-banking financial institution lends and issues a cheque on its bank

as payment.

This will lead to a drain on its resources unless an equal

amount is re-deposited by some other borrower. In the case of small NBFIs, the

redeposit ratio is low which makes it difficult for them to continue in

business unless they have sufficient assets. But a commercial bank faces no

problem of this type and can create money as well as liquidity to meet its

lending requirements.

2. Cash Reserve Requirements:

Commercial banks, like other FIs, have to earn a higher rate

on their total assets than they pay on their total liabilities. They have to

keep cash reserves. But cash reserves do not earn income. So banks wish to

maintain their cash reserves as low as possible. But, unlike NBFIs, they are

legally required to maintain a minimum cash reserve ratio (CRR).

This ratio is always more than what the banks would wish to

maintain. As a result, banks do not normally hold cash reserves in excess of

those legally required and invest all excess cash in earning assets. With a

reduction of required cash reserve ratio, the volume of bank intermediation

would expand, and vice versa.

As deposits are preferred to currency, an increase in the

stock of high powered money results in an increase in the public’s demand for

bank deposits. This leads to increase in deposits with the banking system. So

long as the average cost of providing and servicing demand deposits is low

relative to the interest rate earned on primary securities, banks have a profit

incentive to lend all excess cash by buying securities and granting loans.

Consequently, the volume of bank intermediation expands.

This process will continue until bank assets and deposits have risen to a level

where the required cash reserves and actual reserves are equal.

It should, however, be noted that the foreign exchange

liabilities of commercial banks are not required to meet cash reserve

requirements. So this part of the bank business can be regarded like an NBFI.

On the other hand, NBFIs are not subject to any such restrictions.

They are thus in an advantageous position over the banks.

But this regulatory distinction between banks and NBFIs does not apply now in

almost all the developed and developing countries of the world because reserve

equirements have been enforced in one form or another on NBFIs with the

exception of insurance companies, pension funds, and investment and unit

trusts.

3. Portfolio Structure:

Commercial banks differ from NBFIs in their portfolio

structure. Bank liabilities are very liquid. The liabilities of a bank are

large in relation to its assets, because it holds a small proportion of its

assets in cash. But its liabilities are payable on demand at a short notice.

Many types of assets are available to a bank with varying degree of liquidity.

The most liquid is cash. The next most liquid assets are

deposits with the central bank, treasury bills and other short-term bills

issued by the centre and state governments and large firms, and call loans to

other banks, firms, dealers and brokers in government securities.

The less liquid assets are the various types of loans to

customers and investment in longer-term bonds and mortgages. Thus banks have a

large and varied portfolio on the basis of which they create liquidity.

NBFIs also create liquidity but in the form of savings and

time deposits which are not used as a means of payment. They are limited in the

choice of their assets and are also prohibited from holding certain assets.

Thus the size of their portfolio is very small as compared with banks.

They generally issue claims against themselves that are

fixed in money terms and have maturities shorter than the direct securities

they hold. They borrow for short period, and lend for long period. This is

because of the small size of their portfolio and they hold less liquid assets

than banks.

4. Risk:

Banks have to follow certain norms at the time of advancing

loans. There are detailed appraisals of projects and hence delays in

sanctioning loans. On the other hand, NBFIs do not enter into detailed

appraisals of projects, they have to follow less stringent rules for advances.

There are no time delays in granting loans. Thus NBFIs are able to take greater

risk and lesser supervision as compared to banks.

5. Security:

NBFIs insist on greater security than banks before lending.

Normally, it is in the form of shares and post-dated cheques. This is to ensure

that if one project goes bad, they can recover from the others.

6. Recovery:

NBFIs are very innovative in their methods of recovery and

calculation of interest rates. They combine a good security with other factors

such as upfront fee, and higher lending rates. Consequently, their recovery

rates are good and the percentage of bad debts to their assets is very low.

Banks, on the other hand have to follow specific norms in

making loans. Their prime lending rates are much lower than the NBFIs. Since

banks advance huge loans to corporates, the rate of default is very high in

their case.

Non-Scheduled Banks of Bangladesh:

1. Ansar

VDP Unnayan Bank

2. Jubilee

Bank

3. Karmashangosthan

Bank

4. Palli

Sanchay Bank

5. Grameen

Bank

Scheduled Banks of Bangladesh

1. AB Bank Limited http://www.abbl.com

2. Agrani Bank Limited http://www.agranibank.org

3. Al-Arafah Islami Bank Limited http://www.al-arafahbank.com/

4. Bangladesh Commerce Bank Limited http://bcblbd.com/

5. Bangladesh Development Bank Limited http://www.bdbl.com.bd

6. Bangladesh Krishi Bank http://www.krishibank.org.bd

7. Bank Al-Falah Limited http://www.bankalfalah.com

8. Bank Asia Limited http://www.bankasia-bd.com

9. BASIC Bank Limited http://www.basicbanklimited.com

10. BRAC Bank Limited http://www.bracbank.com

11. Citibank N.A http://www.citi.com/domain/index.htm

12. Commercial Bank of Ceylon Limited http://www.combank.net/bdweb/

13. Community Bank Bangladesh Limited http://www.communitybankbd.com

14. Dhaka Bank Limited http://dhakabankltd.com

15. Dutch-Bangla Bank Limited http://www.dutchbanglabank.com

16. Eastern Bank Limited http://www.ebl.com.bd

17. EXIM Bank Limited http://www.eximbankbd.com

18. First Security Islami Bank Limited http://www.fsiblbd.com

19. Habib Bank Ltd. http://globalhbl.com/Bangladesh/

20. ICB Islamic Bank Ltd. http://www.icbislamic-bd.com/

21. IFIC Bank Limited http://www.ificbank.com.bd/

22. Islami Bank Bangladesh Ltd http://www.islamibankbd.com

23. Jamuna Bank Ltd http://www.jamunabankbd.com

24. Janata Bank Limited http://www.janatabank-bd.com

25. Meghna Bank Limited http://www.meghnabank.com.bd

26. Mercantile Bank Limited http://www.mblbd.com

27. Midland Bank Limited http://www.midlandbankbd.net/

28. Modhumoti Bank Ltd. http://modhumotibankltd.com/

29. Mutual Trust Bank Limited http://www.mutualtrustbank.com

30. National Bank Limited http://www.nblbd.com

31. National Bank of Pakistan http://www.nbp.com.pk

32. National Credit & Commerce Bank

Ltd http://www.nccbank.com.bd

33. NRB Bank Limited http://www.nrbbankbd.com

34. NRB Commercial Bank Limited http://www.nrbcommercialbank.com/

35. NRB Global Bank Limited http://www.nrbglobalbank.com

36. One Bank Limited http://www.onebankbd.com

37. Padma Bank Limited http://www.padmabankbd.com/

38. Premier Bank Limited http://www.premierbankltd.com

39. Prime Bank Ltd https://www.primebank.com.bd/

40. Probashi Kollyan Bank http://www.pkb.gov.bd/

41. Pubali Bank Limited http://www.pubalibangla.com

42. Rajshahi Krishi Unnayan Bank http://www.rakub.org.bd

43. Rupali Bank Limited https://rupalibank.org/en/

44. Shahjalal Islami Bank Limited http://www.sjiblbd.com/

45. Shimanto Bank Limited https://www.shimantobank.com/

46. Social Islami Bank Ltd. http://www.siblbd.com

47. Sonali Bank Limited http://www.sonalibank.com.bd

48. South Bangla Agriculture &

Commerce Bank Limited http://www.sbacbank.com/

49. Southeast Bank Limited https://www.southeastbank.com.bd

50. Standard Bank Limited http://www.standardbankbd.com

51. Standard Chartered Bank http://www.standardchartered.com/bd

52. State Bank of India https://bd.statebank/

53. The City Bank Ltd. http://www.thecitybank.com

54. The Hong Kong and Shanghai Banking

Corporation. Ltd. http://www.hsbc.com.bd

55. Trust Bank Limited http://www.trustbank.com.bd

56. Union Bank Limited http://www.unionbank.com.bd/

57. United Commercial Bank Limited http://www.ucb.com.bd/

58. Uttara Bank Limited http://www.uttarabank-bd.com

59. Woori Bank http://www.wooribank.com

The financial market in Bangladesh

1. Money Market: The money market

comprises banks and financial institutions as intermediaries, 20 of them are

primary dealers in treasury securities. Interbank clean and repo based lending,

BB's repo, reverse repo auctions, BB bills auctions, treasury bills auctions

are primary operations in the money market, there is also active secondary

trade in treasury bills (upto 1 year maturity).

2. Taka Treasury Bond market: The Taka

treasury bond market consists of primary issues of treasury bonds of different

maturities (2, 5, 10, 15 and 20 years), and secondary trade therein through

primary dealers. 20 banks performing as Primary Dealers participate directly in

the primary auctions. Other bank and non bank investors can participate in

primary auctions and in secondary trading through their nominated Primary

Dealers. Non-resident individual and institutional investors can also

participate in primary and secondary market, but only in treasury bonds. Monthly

data on primary and secondary trade volumes in treasury bills and bonds and

data on outstanding volume of treasury bonds held by non residents can be

accessed at Monthly data of Treasury Bills & Bonds .

3. Capital market: The primary issues and

secondary trading of equity securities of capital market take place through two

(02) stock exchanges-Dhaka Stock Exchange and Chittagong Stock Exchange. The

instruments in these exchanges are equity securities (shares), debentures and

corporate bonds. The capital market is regulated by Bangladesh Securities and

Exchange Commission (BSEC).

4. Foreign Exchange Market: Towards

liberalization of foreign exchange transactions, a number of measures were

adopted since 1990s. Bangladeshi currency, the taka, was declared convertible

on current account transactions (as on 24 March 1994), in terms of Article VIII

of IMF Article of Agreement (1994). As Taka is not convertible in capital

account, resident owned capital is not freely transferable abroad. Repatriation

of profits or disinvestment proceeds on non-resident FDI and portfolio investment

inflows are permitted freely. Direct investments of non-residents in the

industrial sector and portfolio investments of non-residents through stock

exchanges are repatriable abroad, as also are capital gains and

profits/dividends thereon. Investment abroad of resident-owned capital is

subject to prior Bangladesh Bank approval, which is allowed only sparingly.

Bangladesh adopted Floating Exchange Rate regime since 31 May 2003. Under the

regime, BB does not interfere in the determination of exchange rate, but

operates the monetary policy prudently for minimizing extreme swings in

exchange rate to avoid adverse repercussion on the domestic economy. The

exchange rate is being determined in the market on the basis of market demand

and supply forces of the respective currencies. In the forex market banks are

free to buy and sale foreign currency in the spot and also in the forward

markets. However, to avoid any unusual volatility in the exchange rate,

Bangladesh Bank, the regulator of foreign exchange market remains vigilant over

the developments in the foreign exchange market and intervenes by buying and

selling foreign currencies whenever it deems necessary to maintain stability in

the foreign exchange market.

Regulators of the Financial System

Central

Bank

Bangladesh

Bank acts as the Central Bank of Bangladesh which was established on December

16, 1971 through the enactment of Bangladesh Bank Order 1972- President’s Order

No. 127 of 1972 (Amended in 2003).

The

general superintendence and direction of the affairs and business of BB have

been entrusted to a 9 members' Board of Directors which is headed by the

Governor who is the Chief Executive Officer of this institution as well. BB has

45 departments and 10 branch offices.

In

Strategic Plan (2010-2014), the vision of BB has been stated as, “To develop

continually as a forward looking central bank with competent and committed

professionals of high ethical standards, conducting monetary management and

financial sector supervision to maintain price stability and financial system

robustness, supporting rapid broad based inclusive economic growth, employment

generation and poverty eradication in Bangladesh”.

The

main functions of BB are (Section 7A of BB Order, 1972) -

1. to formulate and implement monetary

policy;

2. to formulate and implement

intervention policies in the foreign exchange market;

3. to give advice to the Government on

the interaction of monetary policy with fiscal and exchange rate policy, on the

impact of various policy measures on the economy and to propose legislative

measures it considers necessary or appropriate to attain its objectives and

perform its functions;

4. to hold and manage the official

foreign reserves of Bangladesh;

5. to promote, regulate and ensure a

secure and efficient payment system, including the issue of bank notes;

6. to regulate and supervise banking

companies and financial institutions.

Core

Policies of Central Bank

Monetary

policy

The

main objectives of monetary policy of Bangladesh Bank are:

a. Price

stability both internal & external

b. Sustainable

growth & development

c. High

employment

d. Economic and

efficient use of resources

e. Stability of

financial & payment system

Bangladesh

Bank declares the monetary policy by issuing Monetary Policy Statement (MPS)

twice (January and July) in a year. The tools and instruments for

implementation of monetary policy in Bangladesh are Bank Rate, Open Market

Operations (OMO), Repurchase agreements (Repo) & Reverse Repo, Statutory

Reserve Requirements (SLR & CRR).

Reserve

Management Strategy

Bangladesh

Bank maintains the foreign exchange reserve of the country in different

currencies to minimize the risk emerging from widespread fluctuation in

exchange rate of major currencies and very irregular movement in interest rates

in the global money market. BB has established Nostro account arrangements with

different Central Banks. Funds accumulated in these accounts are invested in

Treasury bills, repos and other government papers in the respective currencies.

It also makes investment in the form of short term deposits with different high

rated and reputed commercial banks and purchase of high rated

sovereign/supranational/corporate bonds. A separate department of BB performs

the operational functions regarding investment which is guided by investment

policy set by the BB's Investment Committee headed by a Deputy Governor. The

underlying principle of the investment policy is to ensure the optimum return

on investment with minimum market risk.

Interest

Rate Policy

Under

the Financial sector reform program, a flexible interest policy was formulated.

According to that, banks are free to charge/fix their deposit (Bank /Financial

Institutes) and Lending (Bank /Financial Institutes) rates other than Export

Credit. At present, except Pre-shipment

export credit and agricultural lending, there is no interest rate cap on

lending for banks. Yet, banks can differentiate interest rate up to 3%

considering comparative risk elements involved among borrowers in same lending

category. With progressive deregulation of interest rates, banks have been

advised to announce the mid-rate of the limit (if any) for different sectors

and the banks may change interest 1.5% more or less than the announced mid-rate

on the basis of the comparative credit risk. Banks upload their deposit and

lending interest rate in their respective website.

Capital

Adequacy for Banks and FIs

Basel-III

has been introduced with a view to strenghening the capital base of banks with

the goal of promoting a more resilient banking sector. The Basel III regulation

will be adopted in a phased manner starting from the January 2015, with full

implementation of capital ratios from the beginning of 2019. Now, scheduled

banks in Bangladesh are required to maintain minimum capital of Taka 4 billion

or Capital to Risk Weighted Assets Ratio (CRAR) 10%, whichever is higher. In

addition to minimum CRAR, Capital Conservation Buffer (CCB) of 2.5% of the

total RWA is being introduced which will be maintained in the form of CET1.

Besides the minimum requirement all banks have a process for assessing overall

capital adequacy in relation to their risk profile and a strategy for

maintaining capital at an adequate level.

For

FIs, full implementation of Basel-II has been started in January 01, 2012

(Prudential Guidelines on Capital Adequacy and Market Discipline (CAMD) for

Financial Institutions). Now, FIs in Bangladesh are required to maintain Tk. 1

billion or 10% of Total Risk Weighted Assets as capital, whichever is higher.

Deposit

Insurance

The

deposit insurance scheme (DIS) was introduced in Bangladesh in August 1984 to

act as a safety net for the depositors. All the scheduled banks Bangladesh are

the member of this scheme Bank Deposit Insurance Act 2000. The purpose of DIS

is to help to increase market discipline, reduce moral hazard in the financial

sector and provide safety nets at the minimum cost to the public in the event

of bank failure. A Deposit Insurance Trust Fund (DITF) has also been created

for providing limited protection (not exceeding Taka 0.01 million) to a small

depositor in case of winding up of any bank. The Board of Directors of BB is

the Trustee Board for the DITF. BB has adopted a system of risk based deposit

insurance premium rates applicable for all scheduled banks effective from

January - June 2007. According to new instruction regarding premium rates,

problem banks are required to pay 0.09 percent and private banks other than the

problem banks and state owned commercial banks are required to pay 0.07 percent

where the percent coverage of the deposits is taka one hundred thousand per

depositor per bank. With this end in view, BB has already advised the banks for

bringing DIS into the notice of the public through displaying the same in their

display board.

Insurance

Authority

Insurance

Development and Regulatory Authority (IDRA) was instituted on January 26, 2011

as the regulator of insurance industry being empowered by Insurance Development

and Regulatory Act, 2010 by replacing its predecessor, Chief Controller of

Insurance. This institution is operated under Ministry of Finance and a 4

member executive body headed by Chairman is responsible for its general

supervision and direction of business.

IDRA

has been established to make the insurance industry as the premier financial

service provider in the country by structuring on an efficient corporate

environment, by securing embryonic aspiration of society and by penetrating

deep into all segments for high economic growth. The mission of IDRA is to

protect the interest of the policy holders and other stakeholders under

insurance policy, supervise and regulate the insurance industry effectively,

ensure orderly and systematic growth of the insurance industry and for matters

connected therewith or incidental thereto.

Regulator

of Capital Market Intermediaries

Securities

and Exchange Commission (SEC) performs the functions to regulate the capital

market intermediaries and issuance of capital and financial instruments by

public limited companies. It was established on June 8, 1993 under the

Securities and Exchange Commission Act, 1993. A 5 member commission headed by a

Chairman has the overall responsibility to administer securities legislation

and the Commission is attached to the Ministry of Finance.

The

mission of SEC is to protect the interests of securities investors, to develop

and maintain fair, transparent and efficient securities markets and to ensure

proper issuance of securities and compliance with securities laws. The main

functions of SEC are:

1. Regulating

the business of the Stock Exchanges or any other securities market.

2. Registering

and regulating the business of stock-brokers, sub-brokers, share transfer

agents, merchant bankers and managers of

issues, trustee of trust deeds, registrar of an issue, underwriters,

portfolio managers, investment advisers and other intermediaries in the

securities market.

3. Registering,

monitoring and regulating of collective investment scheme including all forms

of mutual funds.

4. Monitoring

and regulating all authorized self regulatory organizations in the securities market.

5. Prohibiting

fraudulent and unfair trade practices in any securities market.

6. Promoting

investors’ education and providing training for intermediaries of the

securities market.

7. Prohibiting

insider trading in securities.

8. Regulating

the substantial acquisition of shares and take-over of companies.

9. Undertaking

investigation and inspection, inquiries and audit of any issuer or dealer of

securities, the Stock Exchanges and

intermediaries and any self regulatory organization in the securities

market.

10. Conducting

research and publishing information.

Regulator of Micro Finance

Institutions

To bring Non-government Microfinance

Institutions (NGO-MFIs) under a regulatory framework, the Government of

Bangladesh enacted "Microcredit Regulatory Authority Act, 2006’" (Act

no. 32 of 2006) which came into effect from August 27, 2006. Under this Act,

the Government established Microcredit Regulatory Authority (MRA) with a view

to ensuring transparency and accountability of microcredit activities of the

NGO-MFIs in the country. The Authority is empowered and responsible to

implement the said act and to bring the microcredit sector of the country under

a full-fledged regulatory framework. MRA’s mission is to ensure transparency

and accountability of microfinance operations of NGO-MFIs as well as foster

sustainable growth of this sector. In order to achieve its mission, MRA has set

itself the task to attain the following goals:

1. To formulate

as well as implement the policies to ensure good governance and transparent financial

systems of MFIs.

2. To conduct

in-depth research on critical microfinance issues and provide policy inputs to

the government consistent with the national strategy for poverty eradication.

3. To provide

training of NGO-MFIs and linking them with the broader financial market to

facilitate sustainable resources and efficient management.

4. To assist

the government to build up an inclusive financial market for economic

development of the country.

5. To identify

the priorities in the microfinance sector for policy guidance and dissemination

of information to attain the MRA’s social responsibility.

According

to the Act, the MRA will be responsible for the three primary functions that

will need to be carried out, namely:

1. Licensing of

MFIs with explicit legal powers;

2. Supervision

of MFIs to ensure that they continue to comply with the licensing requirements;

and

3. Enforcement

of sanctions in the event of any MFI failing to meet the licensing and ongoing

supervisory requirements.

Capital Market

After the independence, establishment of Dhaka

Stock Exchange (formerly East Pakistan Stock Exchange) initiated the pathway of

capital market intermediaries in Bangladesh. In 1976, formation of Investment

Corporation of Bangladesh opened the door of professional portfolio management

in institutional form. In last two decades, capital market witnessed number of

institutional and regulatory advancements which has resulted diversified

capital market intermediaries. At present, capital market intermediaries are of

following types:

1. Stock Exchanges:

Apart from Dhaka Stock Exchange, there is another stock exchange in Bangladesh

that is Chittagong Stock Exchange established in 1995.

2. Central

Depository: The only depository system for the transaction and settlement of

financial securities, Central Depository Bangladesh Ltd (CDBL) was formed in

2000 which conducts its operations under Depositories Act 1999, Depositories

Regulations 2000, Depository (User) Regulations 2003, and the CDBL by-laws.

3. Stock

Dealer/Sock Broker: Under SEC (Stock Dealer, Stock Broker & Authorized

Representative) Rules 2000, these entities are licensed and they are bound to

be a member of any of the two stock exchanges. At present, DSE and CSE have 238

and 136 members respectively.

4. Merchant

Banker & Portfolio Manager: These institutions are licensed to operate

under SEC (Merchant Banker & Portfolio Manager Rules) 1996 and 45

institutions have been licensed by SEC under this rules so far.

5. Asset

Management Companies (AMCs): AMCs are authorized to act as issue and portfolio

manager of the mutual funds which are issued under SEC (Mutual Fund) Rules

2001. There are 15 AMCs in Bangladesh at present.

6. Credit

Rating Companies (CRCs): CRCs in Bangladesh are licensed under Credit Rating

Companies Rules, 1996 and now, 5 CRCs have been accredited by SEC.

7. Trustees/Custodians:

According to rules, all asset backed securitizations and mutual funds must have

an accredited trusty and security custodian. For that purpose, SEC has licensed

9 institutions as Trustees and 9 institutions as custodians.

8. Investment

Corporation of Bangladesh (ICB): ICB is a specialized capital market

intermediary which was established in 1976 through the ordainment of The

Investment Corporation of Bangladesh Ordinance 1976. This ordinance has

empowered ICB to perform all types of capital market intermediation that fall

under jurisdiction of SEC. ICB has three subsidiaries:

8.1. ICB Capital Management

Ltd.,

8.2. ICB Asset Management Company Ltd.,

8.3. ICB Securities Trading Company Ltd.

8.2. ICB Asset Management Company Ltd.,

8.3. ICB Securities Trading Company Ltd.

Recent Developments in Financial Sector in

Bangladesh

Automation

and Technological Development:

Banking

sector experienced remarkable progress in respect of automation in functioning

in last several years. For the pro-active and forward-visioning approach of

Bangladesh Bank, numbers of automation initiatives have been implemented in

banking sector. These initiatives include:

Bangladesh

introduced the Market Infrastructure (MI) Module for automated auction and

trading of government securities.

To create

a disciplined environment for borrowing, the automated Credit Information

Bureau (CIB) service provides credit related information for prospective and

existing borrowers. With this improved and efficient system, risk management

will be more effective. Banks and financial institutions may furnish credit

information to CIB database 24 by 7 around the year; and they can access credit

reports from CIB online instantly.

L/C

Monitoring System has been introduced for preservation and using the all

necessary information regarding L/C by the banks through BB website. This

system allows the authorized users of banks to upload and download their L/C

information.

In terms

of article 36(3) of Bangladesh Bank Order, 1972, all scheduled banks are

subject to submit Weekly Statement of Position as at the close of business on

every Thursday to the Department of Off-site Supervision. This statement now is

submitted through on-line using the web upload service of BB website within o3

(three) working days after the reporting date which is much more time and labor

efficient that the earlier manual system.

The

e-Returns service has been introduced which is An Online Portal Service for

Scheduled Banks to submit Electronic Returns using predefined template for the

purpose of Macro Economy Analysis through related BB Departments.

Online

Export Monitoring System is used for monitoring export of Bangladesh. Through

this service, Banks and AD Branches of Banks issue & reports export report.

Bangladesh

Automated Clearing House (BACH) started to work by replacing the ancient manual

clearing system which allows the inter-bank cheques and similar type

instruments to be to settled in instant manner.

Electronic

Fund Transfer (EFT) has been introduced which facilitates the banks to make

bulk payments instantly and using least paper and manpower.

The

initiation of Mobile Banking has been one of the most noteworthy advancement in

banking. Through this system, franchises of banks through mobile operators can

provide banking service to even the remotest corner of the country.

Almost every

commercial bank is now using their own core banking solution which has made

banking very faster and efficient. Usage of plastic money has much more

increased in daily life transactions. Full or partial online banking is now

being practiced by almost every bank.

Inauguration

of internet trading in both of the bourses (DSE & CSE) in the country is

the most significant advancement for capital market in last several years.

Micro Finance Institutions submit their reports to the regulator through the

Online Report Submission Tools for MFIs.

Institutional

Development:

Through

the Central Bank Strengthening Project, there have been a good number of

achievements regarding the institutional development in BB which can be

observed below:

The

implementation of Enterprise Resource Planning (ERP) has been a big step in

automation of operational structure of BB.

The

establishment of Enterprise Data Warehouse (under process) will bring the whole

banking and FI industry under a single network through which data sharing,

reporting and supervision will enter in a new horizon.

Bangladesh

Bank now possesses the most informative and resourceful website of the country

regarding economic and financial information.

Internal

networking system with required online communication facilities have been

developed and in operation for the officers of BB.

BB has

hosted number of international seminars on different economic and financial

issues over last several years.

MRA was

established in 2006 for bringing NGO-MFIs under supervision. For the pro active

role of MRA, this sector (MFI) is now in a good shape regarding the

accountability and regulation.

For

abolishing anomaly and fetching discipline in insurance industry, IDRA was

established in 2011. In one year, IDRA has taken number of appreciable steps to

regularize this industry.

After the

massive crash of local bourses in 2010-2011, the executive body of SEC was

redesigned in full and some good results have come after that.

Regulatory Development:

Banking

and FI industries have experienced diversified regulatory development over last

few years:

1. Basel-III has been introduced in a

phased manner starting from the January 2015, with full implementation of

capital ratios from the beginning of 2019.

2. Guidelines on Environmental and

Climate Change Risk Management for banks and FIs have been circulated. Policy

guidelines on Green Banking also have been issued.

3. Guidelines on Stress Testing for banks

and FIs have been issued which is aimed to assess the resilience of banks and

FIs under different adverse situations.

4. Number of Policy initiatives for

Financial Inclusion has been undertaken.

5. Banks have been asked to build up

separate Risk Management Unit for comprehensive and intensive risk management.

6. Banks have been instructed to create

separate subsidiary for capital market operations and capital market operations

of banks are now minutely monitored.

7. Supervision has been intensified to

increase the participation of banks in Corporate Social Responsibility (CSR).

8. For the efficient and timely action of

BB, foreign exchange reserve of Bangladesh did not face any adversity during

global financial turmoil of 2007-09.

9. To meet international standard on Anti

Money Laundering (AML)/Combating Financing of Terrorism (CFT) issues,

guidelines for Money Changers, Insurance Companies and Postal Remittance have

already been circulated.

10. SEC has updated Public Issue Rules,

2006 and Mutual Fund Rules, 2001. Apart from that, numbers of AMCs, merchant

banks and are Mutual Funds are permitted by SEC which has increased the

participation of institutional investors. The trend of capital market research

has been upward which indicates the potential of analytical investment

decision.

Insurance

Act 2010 was formulated to meet demand of concurrent time for shifting the

insurance industry in a better shape. Apart from that, several initiatives have

been undertaken by IDRA for prohibiting the malpractices in the industry

regarding insurance commission, agent, premium etc and corporate governance

issues.

Insurance

Insurance sector

in Bangladesh emerged after independence with 2 nationalized insurance

companies- 1 Life & 1 General; and 1 foreign insurance company. In mid 80s,

private sector insurance companies started to enter in the industry and it got

expanded. Now days, 62 companies are operating under Insurance Act 2010. Out of

them-

18 are

Life Insurance Companies including 1 foreign company and 1 is state-owned

company,

44 General

Insurance Companies including 1 state-owned company.

Insurance

companies in Bangladesh provide following services:

Life

insurance,

General

Insurance,

Reinsurance,

Micro-insurance,

Takaful or

Islami insurance.

NBFI

Non Bank

Financial Institutions (FIs) are those types of financial institutions which

are regulated under Financial Institution Act, 1993 and controlled by

Bangladesh Bank. Now, 34 FIs are operating in Bangladesh while the maiden one

was established in 1981. Out of the total, 2 is fully government owned, 1 is

the subsidiary of a SOCB, 15 were initiated by private domestic initiative and

15 were initiated by joint venture initiative. Major sources of funds of FIs

are Term Deposit (at least three months tenure), Credit Facility from Banks and

other FIs, Call Money as well as Bond and Securitization.

The major

difference between banks and FIs are as follows:

FIs cannot

issue cheques, pay-orders or demand drafts.

FIs cannot

receive demand deposits,

FIs cannot

be involved in foreign exchange financing,

FIs can

conduct their business operations with diversified financing modes like

syndicated financing, bridge financing, lease financing, securitization

instruments, private placement of equity etc.

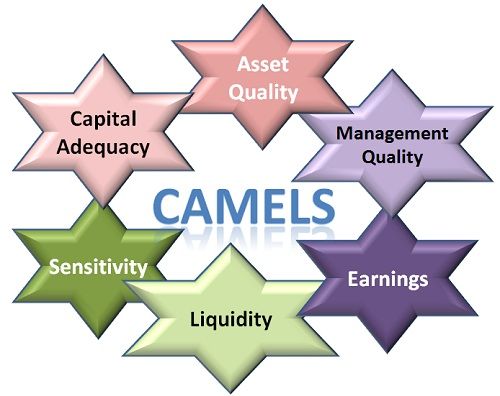

CAMELS

CAMELS

Rating is the

rating system wherein the bank regulators or examiners (generally the officers

trained by RBI), evaluates an overall performance of the banks and determine

their strengths and weaknesses.

CAMELS

Rating is based on the financial statements of the banks, Viz. Profit and loss

account, balance sheet and on-site examination by the bank regulators. In this

Rating system, the officers rate the banks on a scale from 1 to 5, where 1 is

the best and 5 is the worst. The

parameters on the basis of which the ratings are done are represented by an

acronym “CAMELS”.

{kind=link}

1. Capital Adequacy: The capital adequacy measures

the bank’s capacity to handle the losses and meet all its obligations towards

the customers without ceasing its operations.This can be met only on the basis

of an amount and the quality of capital, a bank can access. A ratio of Capital

to Risk Weighted Assets determines the bank’s capital adequacy.

2. Asset Quality: An asset represents all the assets of

the bank, Viz. Current and fixed, loans, investments, real estates and all the

off-balance sheet transactions. Through this indicator, the performance of an

asset can be evaluated. The ratio of Gross Non-Performing Loans to

Gross Advances is one of the criteria to evaluate the effectiveness of

credit decisions made by the bankers.

3. Management Quality: The board of directors and top-level

managers are the key persons who are responsible for the successful functioning

of the banking operations. Through this parameter, the effectiveness of the

management is checked out such as, how well they respond to the changing market

conditions, how well the duties and responsibilities are delegated, how well

the compensation policies and job descriptions are designed, etc.

4. Earnings: Income from all the operations,

non-traditional and extraordinary sources constitute the earnings of a bank.

Through this parameter, the bank’s efficiency is checked with respect to its

capital adequacy to cover all the potential losses and the ability to pay off

the dividends.Return on Assets Ratio measures the earnings of the

banks.

5. Liquidity: The bank’s ability to convert assets

into cash is called as liquidity. The ratio of Cash maintained by Banks

and Balance with the Central Bank to Total Assets determines the

liquidity of the bank.

6. Sensitivity to Market Risk: Through this parameter, the

bank’s sensitivity towards the changing market conditions is checked, i.e. how

adverse changes in the interest rates, foreign exchange rates, commodity

prices, fixed assets will affect the bank and its operations.

Thus,

through CAMELS rating, the overall financial position of the bank is evaluated

and the corrective actions, if any, are taken accordingly.

What Is Market Risk?

Market

risk is the possibility of an investor experiencing losses due to factors that

affect the overall performance of the financial markets in which he or she is

involved. Market risk, also called "systematic risk," cannot be

eliminated through diversification, though it can be hedged against in other

ways. Sources of market risk include recessions, political turmoil, changes in

interest rates, natural disasters and terrorist attacks. Systematic, or market

risk tends to influence the entire market at the same time.

This can

be contrasted with unsystematic risk, which is unique to a specific company or

industry. Also known as “nonsystematic risk,” "specific risk,"

"diversifiable risk" or "residual risk," in the context of

an investment portfolio, unsystematic risk can be reduced through diversification.

Understanding

Market Risk: Market (systematic) risk and specific risk (unsystematic) make up

the two major categories of investment risk. The most common types of market

risks include interest rate risk, equity risk, currency risk and commodity risk.

Publicly

traded companies in the United States are required by the Securities and

Exchange Commission (SEC) to disclose how their productivity and results may be

linked to the performance of the financial markets. This requirement is meant

to detail a company's exposure to financial risk. For example, a company

providing derivative investments or foreign exchange futures may be more

exposed to financial risk than companies that do not provide these types of

investments. This information helps investors and traders make decisions based

on their own risk management rules.

In

contrast to market risk, specific risk or "unsystematic risk" is tied

directly to the performance of a particular security and can be protected

against through investment diversification. One example of unsystematic risk is

a company declaring bankruptcy, thereby making its stock worthless to

investors.

Main Types

of Market Risk: Interest rate risk covers the volatility that may accompany

interest rate fluctuations due to fundamental factors, such as central bank

announcements related to changes in monetary policy. This risk is most relevant

to investments in fixed-income securities, such as bonds.

Equity

risk is the risk involved in the changing prices of stock investments, and

commodity risk covers the changing prices of commodities such as crude oil and

corn.

Currency

risk, or exchange-rate risk, arises from the change in the price of one

currency in relation to another; investors or firms holding assets in another

country are subject to currency risk.

Volatility

and Hedging Market Risk: Market risk exists because of price changes. The

standard deviation of changes in the prices of stocks, currencies or

commodities is referred to as price volatility. Volatility is rated in annualized

terms and may be expressed as an absolute number, such as $10, or a percentage

of the initial value, such as 10%.

Investors

can utilize hedging strategies to protect against volatility and market risk.

Targeting specific securities, investors can buy put options to protect against

a downside move, and investors who want to hedge a large portfolio of stocks

can utilize index options.

Measuring

Market Risk: To measure market risk, investors and analysts use the

value-at-risk (VaR) method. VaR modeling is a statistical risk management

method that quantifies a stock or portfolio's potential loss as well as the

probability of that potential loss occurring. While well-known and widely

utilized, the VaR method requires certain assumptions that limit its precision.

For example, it assumes that the makeup and content of the portfolio being

measured is unchanged over a specified period. Though this may be acceptable

for short-term horizons, it may provide less accurate measurements for

long-term investments.

Beta is

another relevant risk metric, as it measures the volatility or market risk of a

security or portfolio in comparison to the market as a whole; it is used in the

capital asset pricing model (CAPM) to calculate the expected return of an

asset.

What Is a Nonperforming Loan?

A

nonperforming loan (NPL) is a sum of borrowed money upon which the debtor has

not made the scheduled payments for a specified period. Although the exact

elements of nonperformance status vary, depending on the specific loan's terms,

"no payment" is usually defined as zero payments of either principal

or interest. The specified period also varies, depending on the industry and

the type of loan. Generally, however, the period is 90 days or 180 days.

How a

Nonperforming Loan Works

A

nonperforming loan (NPL) is considered in default or close to default. Once a

loan is nonperforming, the odds the debtor will repay it in full are

substantially lower. If the debtor resumes payments again on an NPL, it becomes

a reperforming loan, even if the debtor has not caught up on all the missed

payments.

In

banking, commercial loans are considered nonperforming if the debtor has made

zero payments of interest or principal within 90 days, or is 90 days past due.

For a consumer loan, 180 days past due classifies it as an NPL.

KEY

TAKEAWAYS

A

nonperforming loan (NPL) is a loan in which the borrower hasn't made any

scheduled payments of principal or interest for some time.

In

banking, commercial loans are considered nonperforming if the borrower is 90

days past due.

The

International Monetary Fund considers loans that are less than 90 days past due

as nonperforming if there's high uncertainty surrounding future payments.

Types of

Nonperforming Loans

A debt can

achieve "nonperforming loan" status in several ways. Examples of NPLs

include:

A loan in

which 90 days' worth of interest has been capitalized, refinanced, or delayed

due to an agreement or an amendment to the original agreement.

A loan in

which payments are less than 90 days late, but the lender no longer believes

the debtor will make future payments.

A loan in

which the maturity date of principal repayment has occurred, but some fraction

of the loan remains outstanding.

Official

Definitions of Nonperforming Loans

Several

international financial authorities offer specific guidelines for determining

nonperforming loans.

The

European Central Bank: The European Central Bank (ECB) requires asset and

definition comparability to evaluate risk exposures across euro area central

banks. The ECB specifies multiple criteria that can cause an NPL classification

when it performs stress tests on participating banks.

In 2014,

the ECB performed a comprehensive assessment and developed criteria to define

loans as nonperforming if they are:

90 days

past due, even if they are not defaulted or impaired

Impaired

with respect to the accounting specifics for U.S. GAAP and International

Financial Reporting Standards (IFRS) banks

In default

according to the Capital Requirements Regulation

An

addendum, issued in 2018, specified the time frame for lenders to set aside

funds to cover nonperforming loans: two to seven years, depending on whether

the loan was secured or not. As of 2019, eurozone lenders still have

approximately $990 billion worth of nonperforming loans on their books.

A nonperforming loan (NPL) is one in which

payments of either interest or principal have not been made for a set number of

days, for whatever reason.

The

International Money Fund

The

International Monetary Fund (IMF) also sets out multiple criteria for a

nonperforming loan classification.

In 2005,

the IMF defined nonperforming loans as loans whose:

Debtors

have not paid interest and/or principal payments in at least 90 days or more

Interest

payments equal to 90 days or more have been capitalized, refinanced, or delayed

by agreement

Payments

have been delayed by less than 90 days, but come with high uncertainty or no

certainty the debtor will make payments in the future

What is Funds Management

Funds

management is the overseeing and handling of a financial institution's cash

flow. The fund manager ensures that the maturity schedules of the deposits

coincide with the demand for loans. To do this, the manager looks at both the

liabilities and the assets that influence the bank's ability to issue credit.

BREAKING

DOWN Funds Management

Funds

management – also referred to as asset management – covers any kind of system

that maintains the value of an entity. It may be applied to intangible assets

(e.g., intellectual property and goodwill), and tangible assets (e.g.,

equipment and real estate). It is the systematic process of operating,

deploying, maintaining, disposing, and upgrading assets in the most

cost-efficient and profit-yielding way possible.

A fund

manager must pay close attention to cost and risk to capitalize on the cash

flow opportunities. A financial institution runs on the ability to offer credit

to customers. Ensuring the proper liquidity of the funds is a crucial aspect of

the fund manager's position. Funds management can also refer to the management

of fund assets.

In the

financial world, the term "fund management" describes people and

institutions that manage investments on behalf of investors. An example would

be investment managers who fix the assets of pension funds for pension

investors.

Fund

management may be divided into four industries: the financial investment

industry, the infrastructure industry, the business and enterprise industry,

and the public sector.

Financial

Fund Management: The most common use of "fund management" refers to

investment management or financial management, which are within the financial

sector responsible for managing investment funds for client accounts. The fund

manager's duties include studying the client's needs and financial goals, creating

an investment plan, and executing the investment strategy.

Classifying

Fund Management: Fund management can be classified according to client type,

the method used for management, or the investment type.

When

classifying fund management according to client type, the fund managers are

either business fund managers, corporate fund managers, or personal fund

managers who handle investment accounts for individual investors. Personal fund

managers cover smaller investment portfolios compared to business fund

managers. These funds may be controlled by one fund manager or by a team of

many fund managers.

Some funds

are managed by hedge fund managers who earn from an upfront fee and a certain

percentage of the fund's performance, which serves as an incentive for them to

perform to the best of their abilities.

Liquidity Management in Business and Investing

Liquidity

management takes one of two forms based on the definition of liquidity. One

type of liquidity refers to the ability to trade an asset, such as a stock or

bond, at its current price. The other definition of liquidity applies to large

organizations, such as financial institutions. Banks are often evaluated on

their liquidity, or their ability to meet cash and collateral obligations

without incurring substantial losses. In either case, liquidity management

describes the effort of investors or managers to reduce liquidity risk

exposure.

Liquidity

Management in Business

Investors,

lenders, and managers all look to a company's financial statements using liquidity

measurement ratios to evaluate liquidity risk. This is usually done by

comparing liquid assets and short-term liabilities, determining if the company

can make excess investments, pay out bonuses or, meet their debt obligations.

Companies that are over-leveraged must take steps to reduce the gap between

their cash on hand and their debt obligations. When companies are

over-leveraged, their liquidity risk is much higher because they have fewer

assets to move around.

All

companies and governments that have debt obligations face liquidity risk, but

the liquidity of major banks is especially scrutinized. These organizations are

subjected to heavy regulation and stress tests to assess their liquidity

management because they are considered economically vital institutions. Here,

liquidity risk management uses accounting techniques to assess the need for

cash or collateral to meet financial obligations. The Dodd-Frank Wall Street

Reform and Consumer Protection Act passed in 2010 raised these requirements much

higher than they were before the 2008 Financial Crisis. Banks are now required

to have a much higher amount of liquidity, which in turn lowers their liquidity

risk.

Liquidity

Management in Investing

Investors

still use liquidity ratios to evaluate the value of a company's stocks or

bonds, but they also care about a different kind of liquidity management. Those

who trade assets on the stock market cannot just buy or sell any asset at any

time; the buyers need a seller, and the sellers need a buyer.

When a

buyer cannot find a seller at the current price, he or she must usually raise

his or her bid to entice someone to part with the asset. The opposite is true

for sellers, who must reduce their ask prices to entice buyers. Assets that

cannot be exchanged at a current price are considered illiquid. Having the

power of a major firm who trades in large stock volumes increases liquidity

risk, as it is much easier to unload (sell) 15 shares of a stock than it is to

unload 150,000 shares. Institutional investors tend to make bets on companies

that will always have buyers in case they want to sell, thus managing their

liquidity concerns.

Investors

and traders manage liquidity risk by not leaving too much of their portfolios

in illiquid markets. In general, high-volume traders, in particular, want

highly liquid markets, such as the forex currency market or commodity markets

with high trading volumes like crude oil and gold. Smaller companies and

emerging tech will not have the type of volume traders need to feel comfortable

executing a buy order.

What is Prime Security and Collateral Security?

To obtain

Bank Loan borrower has to put some assets as security against the loan amount.

Security protects banker and lender against losses in case of default by the

borrower. Bank has the right to seize the security to recover the dues from the

borrower if the borrower fails to repay the loan amount.

Types of

SecurityThere are two types of Security, such as: Prime Security, Collateral

Security

Prime

Security

Prime

Securities are the assets which are directly related to loan and kept that as

security. So, prime security can be the thing that is being financed. Lender

keeps that assets as prime security for securing the financed amount against

any default by the borrower.

For Example,

in case of housing loan, the house is primary security and in case of term loan

for Plant and Machinery, Plant and Machinery will be primary security.

Collateral

Security

Collateral

Security is the secondary security, is used when Primary Security is not

sufficient to cover the whole loan amount in case of default by the borrower.

This security is the additional security to the Primary Security.

Example of

Prime Security and Collateral Security

Suppose,

you have borrowed a housing loan of USD 2 million from a commercial bank to

acquire a residential flat. The bank asks you to mortgage the same flat against

the loan. This is Called Prime Security.

For

example, Bank finance a term loan of 80 lakh for purchase of machinery to an

industrialist. He purchases machinery

worth 1 crore for his factory. Lender bank put a stipulation for residential

flat as collateral security for the above term loan. So Machinery purchase out

of this term loan is prime security while residential flat is collateral

security.

When

Collateral Security is needed?

In case of Cash credit Limits, Stock and book

debt are primary security. But borrower may sell Stocks and book debts, so bank

requires additional security (collateral) in the form of immovable assets

(building, land) to secure the loan.

In the

case of Housing Loan, Car Loan, and Personal Loan, collateral security is not

required.

Micro

Credit doesn’t need any Collateral Security.

Bank Loans

without collateral are known as collateral free loans.

Primary Security vs Collateral Security

What is

Security?

One of the

major functions of a bank is to provide credit to the customers for various

purposes such as home, vehicle etc and a bank’s strength and solvency depends

on the quality of its loans and advances. Security resembles an insurance

against emergency. It provides a protection to the lender in case of loan

default as the lender could acquire the security if the repayment is not done

by the borrower.

What are

Secured and Unsecured loans?

An

arrangement in which a lender gives money or property to a borrower and the

borrower agrees to return the property or repay the money, usually along with

interest, at some future point in time is called a loan.

A loan can

be broadly classified as a secured and unsecured loan.

Secured

loans

Secured

Loans are those which are protected by some sort of asset or collateral, for

example – mortgage, auto loan, construction loan etc. If the lender is unable

to repay the loan, the borrower has the right to sell off the asset to recover the

loan.

Unsecured

loan

Unsecured

loans include things like credit card purchases, education loan where borrower

don’t have to provide any physical item or valuable assets as security for the

loan. If a person is not able to repay this type of loan it leads to a bad

credit history which creates problems in future when he tries to get a loan

from other lenders or the lender may appoint a collection agency which will use

all its possible tools to recover the amount.

|

Basis for comparison

|

Secured loan

|

Unsecured loan

|

|

Asset

|

Compulsory

|

Not compulsory

|

|

Basis

|

Collateral

|

Creditworthiness

|

|

Risk of loss

|

Very less

|

High

|

|

Tenure

|

Long period

|

Short period

|

|

Borrowing limit

|

High

|

Less

|

|

Rate of interest

|

Low

|

High

|

What is

the importance of Asset/collateral?

For

lender: It reduces the risk associated with the loan default as in the case of

insolvency of the borrower the lender could sell off his asset to compensate

the loss occurred. Moreover, the borrower will make payments if he doesn’t want

to lose his pledged security.

For

borrower: Secured loan has a low rate of interest and give more time to repay

the loan so a borrower with low income can easily afford it. Secondly, if a

borrower has bad credit or limited income, most of the financial institutions

are reluctant in providing a loan but if he pledges collateral, the lender may

be more willing to approve his application.

Types of

security

There are

two types of security

Primary

Security

When an

asset acquired by the borrower under a loan is offered to the lender as

security for the financed amount then that asset is called Primary Security. In

simple terms, it is the thing that is being financed.

Example: A

person takes a housing loan of Rs 50 lakh from the bank and purchases a

residential loan. That flat will be mortgaged to the bank as primary security.

Collateral

Security

If the

bank or financial institution feels that the primary security is not enough to

cover the risk associated with the loan it asks for an additional security

along with primary security which is called Collateral Security. It guarantees

a borrower’s performance on a debt obligation. It can also be issued by a third

party or an intermediary.

Example: A

person takes a loan of Rs 2 crore for the types of machinery. So to secure itself

in the case of default by the borrower it asks for mortgaging residential flat

or hypothecating jewellery, which will be termed as collateral security.

RBI has

advised the banks not to obtain any collateral security in case of all priority

sector advances up to Rs. 25000. In other cases, it is left to the mutual

agreement of the borrower with the bank.

When

collateral security is required?

Collateral

security is not required in housing loan, car loan, personal loan etc. It is

required by lenders in corporate loans like cash credit because in cash credit

primary security such as stock and book debts can be sold any time by the

borrower so an additional security in shape of immovable property or some other

assets are taken to secure loan.

What are

collateral free loans?

Loans that

are disbursed without collateral or security, which limit the lender’s exposure

to risk, are called collateral free loans. This facility is provided under

Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), where

micro and small enterprises can be extended loan upto Rs. 1 crore without

security. This scheme was launched to solve the problem of lack of funding that

these enterprises face as well as to boost their development.

Advantages

No

collateral or third party guarantee is required

The

subsidised rate of interest.

Flexible

repayment tenures up to 5 years.

No track

record required.

Quick and

hassle free processing of applications.

Letter of

credit/bill discounting up to 180 days.

Similarly,

MUDRA (Micro Units Development and Refinance Agency) bank provide

collateral-free financial aid up to Rs. 10 lakhs to sole proprietors or

entrepreneurs carrying on Small and Medium enterprises.

**What is an Offshore Banking Unit (OBU)

An

offshore banking unit (OBU) is a bank shell branch, located in another

international financial center (or, in the case of India, a Special Economic

Zone). Offshore banking units (OBUs) make loans in the Eurocurrency market when

they accept deposits from foreign banks and other OBUs. Local monetary

authorities and governments do not restrict OBUs' activities; however, they are

not allowed to accept domestic deposits or make loans to residents of the

country, in which they are physically situated. Overall OBUs can enjoy

significantly more flexibility regarding national regulations.

BREAKING

DOWN Offshore Banking Unit (OBU)

OBUs have

proliferated across the globe since the 1970s. They are found throughout

Europe, as well as in the Middle East, Asia, and the Caribbean. U.S. OBUs are

concentrated in the Bahamas, the Cayman Islands, Hong Kong, Panama, and

Singapore. In some cases, offshore banking units may be branches of resident

and/or nonresident banks; while in other cases an OBU may be an independent

establishment. In the first case, the OBU is within the direct control of a

parent company; in the second, even though an OBU may take the name of the

parent company, the entity’s management and accounts are separate.

Some

investors may, at times, consider moving money into OBUs to avoid taxation

and/or retain privacy. More specifically, tax exemptions on withholding tax and

other relief packages on activities, such as offshore borrowing, are

occasionally available. In some cases, it is possible to obtain better interest

rates from OBUs. Offshore banking units also often do not have currency

restrictions. This enables them to make loans and payments in multiple

currencies, often opening more flexible international trade options.

History of

Offshore Banking Units

The euro

market allowed the first application of an offshore banking unit. Shortly

afterward Singapore, Hong Kong, India, and other nations followed suit as the

option allowed them to become more viable financial centers. While it took

Australia longer to join, given less favorable tax policies, in 1990, the

nation established more supportive legislation.

In the

United States, the International Banking Facility (IBF) acts as an in-house

shell branch. Its function serves to make loans to foreign customers. As with

other OBUs, IBF deposits are limited to non-U.S applicants.

**What Is Positive Pay?

Positive

pay is an automated cash-management service employed to deter check fraud.

Banks use positive pay to match the checks a company issues with those it

presents for payment. Any check considered suspect is sent back to the issuer

for examination. The system acts as a form of insurance for a company against

fraud, losses, and other liabilities. There is generally a charge incurred for

using it, although some banks now offer the service for free.

KEY

TAKEAWAYS

Positive

pay is a fraud-prevention system offered by most commercial banks to companies

to protect them against forged, altered, and counterfeit checks.

The

company provides a list to the bank of the check number, dollar amount, and

account number of each check.

The bank

compares the list to the actual checks, flags any that do not match, and

notifies the company.

The

company then tells the bank whether or not to cash the check.

Understanding

Positive Pay

In order

to protect against forged, altered, and counterfeit checks, the service matches

the check number, dollar amount, and account number of each check against a

list provided by the company. In some cases the payee may also be included on

the list. If these do not match, the bank will not clear the check. When

security checks are not put in place, identity thieves and fraudsters can

create counterfeit checks that may end up being honored.

When the

information does not match the check, the bank notifies the customer through an

exception report, withholding payment until the company advises the bank to

accept or reject the check. The bank can flag the check, notify a

representative at the company, and seek permission to clear the check. If the

company finds only a slight error or other minor problem, it can choose to

advise the bank to clear the check. If the company forgets to send a list to

the bank, all checks presented that should have been included may be rejected.

As banks

may not be responsible for fraudulent checks, companies should review the

institution’s terms and conditions thoroughly.

Reverse

Positive Pay vs. Positive Pay

A

variation on the positive-pay concept is the reverse positive-pay system. This

system requires the issuer to monitor its checks on its own, making it the company’s

responsibility to alert the bank to decline a check. The bank notifies the

company daily about all presented checks and clears the checks approved by the

company.

Typically,

if the company does not respond within a fairly short time, the bank will go

ahead and cash the check. This method, therefore, is not as reliable and

effective as positive pay, but it is cheaper.

What Is Stress Testing?

Stress

testing is a computer simulation technique used to test the resilience of

institutions and investment portfolios against possible future financial

situations. Such testing is customarily used by the financial industry to help

gauge investment risk and the adequacy of assets, as well as to help evaluate

internal processes and controls. In recent years, regulators have also required

financial institutions to carry out stress tests to ensure their capital

holdings and other assets are adequate.

Stress

Testing for Risk Management

Companies

that manage assets and investments commonly use stress testing to determine

portfolio risk, then set in place any hedging strategies necessary to mitigate

against possible losses. Specifically, their portfolio managers use internal